“In Florida — which continues to make itself a supply magnet with strong demand + the boost from the new Live Local legislation — three markets (Fort Myers, Sarasota, Daytona Beach) are seeing Class C rent cuts around 10-12%. “

Yes, when you build “luxury” new apartments in big numbers, the influx of supply puts downward pressure on rents at all price points — even in the lowest-priced Class C rentals. Here’s evidence of that happening right now:

There are 12 U.S. markets where Class C rents are falling at least 6% year-over-year. What is the common denominator? You guessed it: Supply. All 12 have supply expansion rates ABOVE the U.S. average.

In Florida — which continues to make itself a supply magnet with strong demand + the boost from the new Live Local legislation — three markets (Fort Myers, Sarasota, Daytona Beach) are seeing Class C rent cuts around 10-12%. Not shown on this Top 12 list, but there are three large Florida markets with high supply also seeing Class C rent cuts of 4-5%: Orlando, Jacksonville and Tampa.

Other key markets nationally to highlight: Ultra-high-supplied big markets like Austin, Phoenix, Salt Lake City, Atlanta and Raleigh/Durham are all seeing sizable Class C rent cuts of at least 6%. Small markets on the list include Myrtle Beach, Wilmington NC, Boise and Colorado Springs.

Bear in mind that apartment demand is NOT the issue in any of these markets. They’re all demand magnets. Sure, they’ve seen some moderation / normalization for in-migration and job growth, but they’re still ranking among the national leaders for net absorption.

Simply put: Supply is doing what it’s supposed to do when you add an awful lot of it. It’s a process academics call “filtering” — which happens when higher-income renters in Class B apartments move up into higher-priced new Class A units … and then Class B units see vacancy increase, so they cut rents to lure up Class C renters. And down the line it goes.

But filtering works best when we build a lot of apartments. We didn’t see this phenomenon play out as clearly in past cycles when supply was relatively limited — and (crucially) failed to keep pace with demand.

Less anyone still in doubt, here’s another factoid: Where are Class C rents growing most? You guessed it (I hope!) — in markets with little new supply. Class C rent growth topped 5% in 18 of the nation’s 150 largest metro areas, and nearly all of them have limited new apartment supply. That list includes markets like: Midland/Odessa TX, Knoxville TN, Grand Rapids MI, Dayton OH, Wichita KS, Buffalo NY, Louisville KY, Little Rock AR, and Albany NY.

Among larger markets, Cincinnati and Chicago both saw Class C rent growth near 4% — and both ranked below the U.S. average for new supply.

Most new construction tends to be Class A “luxury” because that’s what pencils out due to high cost of everything from land to labor to materials to impact fees to insurance to taxes, etc.

So critics will say: “We don’t need more luxury apartments!”

Yes, you do. Because when you build “luxury” apartments at scale, you will put downward pressure on rents at all price points.

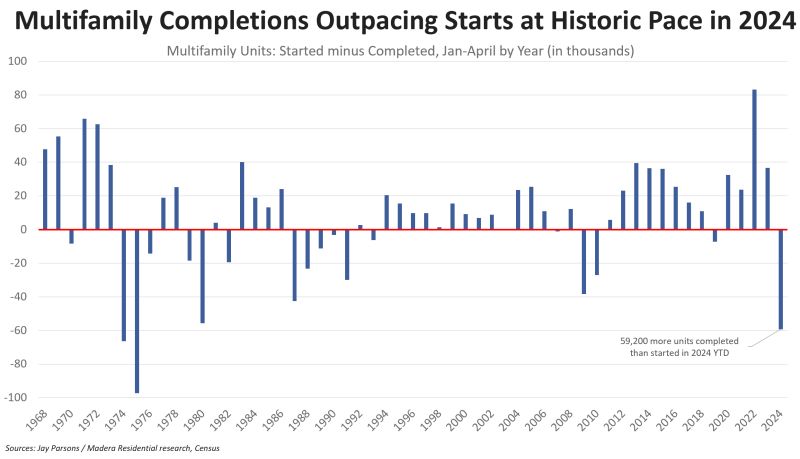

So far here in 2024, U.S. multifamily completions are outpacing new starts at the widest levels since 1975. And that gap is likely to further widen. Ironically: Cheap debt helped fuel the multifamily construction boom, which in turn tamed rental inflation; and expensive debt is helping tame the multifamily construction boom, which could fuel renewed rent inflation.

Through the first four months of 2024, multifamily completions are at multi-decade highs while starts continue to rapidly plunge due to several headwinds: high rates, flat-to-falling rents for lease-ups (depending on the market), and construction costs often coming in above replacement value.

Simply put: It’s very difficult to start new unsubsidized apartment projects right now.

In the short term, supply will likely continue to exceed demand in 2024 — keeping vacancy elevated and putting downward pressure on rents.

In the mid and longer term, you can see how (assuming the job market stays healthy) demand could exceed supply again — perhaps even by next year in some markets, which would in turn put upward pressure on rents (though unlikely to the sky-high growth levels of 2021-22).

It’s difficult to see a scenario where multifamily starts could meaningfully accelerate prior to 2H’25 and more likely in 2026. Even if the Fed trimmed rates a bit, equity and debt players will want to see the current wave of lease-ups stabilize and rent growth return even at moderate levels. Plus, we’ll likely also need to see stabilized asset values rebound enough to bring back the discount to build versus buy (at scale).

The commercial real estate brokers at Bounat work diligently to compile a comprehensive list of the top commercial real estate activity in the Florida region on a frequent basis.

Retail leasing fundamentals in Tampa remain solid despite headwinds caused by continued disruptions in the supply chain and lingering concerns post-pandemic. However, these factors are being counterbalanced with the fact that Florida is the fastest growing state in terms of population in the country, and many people are moving to Tampa specifically.

In general, retail demand in Tampa has been consistently strong over much of the past decade, driven by solid population gains, wage growth, and steady consumer spending. Current vacancy is 3.3%, which is up +0.2% compared to Q3 2023, and the vacancy rate for retail real estate in Tampa remained steady over the past year and is well below the national average, estimated at around 4.5%.

Rent growth has accelerated in recent quarters due to strengthening overall leasing fundamentals following the lifting of some pandemic safeguards. Average asking rents as of Q4 2023 are at $25.56/SF, which is up $0.35 from Q3 2023 when the asking rate was $25.21/SF, up over 2% during the past 3 months (quarter to quarter).

There is currently 563,141 SF of new retail space underway, and nearly 1 million SF has been delivered in the trailing 12-month period. While the pace of new development is falling short of previous years, an uptick in demand bodes well for future development.

Retail investment sales activity over the last year has totaled roughly $1.6 billion in total transaction volume, fueled by considerable investment volume in Q4 and Q2 2022. Q1 2022, from a little over a year ago, still holds records for transaction volume with nearly $600M in retail property sales. It was the second highest quarter of retail real estate sales in the area, illustrating just how feverish investor appetite has been over the last year.

Retail investors continue to target deals in secondary markets like Tampa and Orlando as they seek higher yields, which is becoming harder and harder to achieve. Increased competition for assets is forcing an acceleration in overall retail pricing with the average price per SF growing by 10% year over year and by nearly 15% in the last two years. CoStar’s forecast calls for pricing to continue to rise through 2023 before beginning to level out in early 2024.

The most significant single-property trade over the last year took place in Q2 2023 when the Brandon Town Center (303 – 675 Brandon Town Court) sold for $220M at a price of $296/SF with a vacancy rate of 0% at the time of sale. The Tampa shopping center was built in 1995.

If you would like to discuss the Commercial Real Estate Markets or discuss your asset and its future, let’s connect.

The Nest at Robin’s Apartments will bring 182 new residential units to Bradenton—but unlike other projects going up in the region, these will all be priced as workforce housing. The units will be on a vacant five-acre lot next to Robins Apartments, just south of U.S. 301 on First Street East and east of South Tamiami Trail. Even though groundbreaking is next month and the project will take roughly 18 months to complete, builder and developer One Stop Housing has already received more than 100 applications.

Soaring local rents have made national headlines in recent years and interest rates have increased, making affordable housing a hot topic. It’s gaining some traction with local and state governments, with legislation like the Live Local Act, which, among other points, allows for increases in density and height in exchange for the creation of affordable units. It was recently applied to a downtown Sarasota project that’s still in its early stages.

What’s different about The Nest is that 100 percent of the units will be—and remain—priced for working people, spanning 60 percent to 80 percent of the area median income (AMI).

Units will range from 300 square feet for a studio, (34), to 550 square foot, one-bedroom units (74) and 750 square foot, two-bedroom, two-bathroom units (74).

The studios will be priced at 60 percent of AMI, which amounts to a one-person household earning no more than $42,240 a year. The one and two-bedroom units will be priced at 80 percent of the AMI, which amounts to $64,320 a year for a household of two.

The U.S. Department of Labor released new regulations on Tuesday expanding the scope of fiduciaries in relation to retirement accounts. With the peak of the baby-boom generation in or approaching retirement, rollovers of money from 401(k)s to IRAs are on the rise. Savers move close to $1 trillion each year out of their 401(k) employer-sponsored plans into IRAs and the new regulatory environment will ensure that investments are always in a person’s best interest.

Photo by SD

As a fiduciary ourselves, the regulation is an extension of our business model across financial services. The ruling should better align financial outcomes, lower fees, and decrease lock up requirements – all of which we’re major advocates for. Putting investors first is the ethos of our business and we view the new regulation as a major step towards industry wide best practices.

article via Titan Funds

Refer friends to Smart Cash to earn 6.0%* gross yield for up to 12 months. They’ll earn 6.0%, too. See details.

Home sales for previously owned homes dropped 4.3% in March, and sales were 3.7% lower year over year. Although inventory improved significantly during the month, less people are buying homes due to increasing mortgage rates. All-cash purchases account for 28% of home sales, as more buyers are avoiding loans all together.

Today’s pool of prospective homebuyers has shrunk compared to previous generations – more debt and higher housing costs have made it difficult to afford a first home. In 2020, 2% interest rates drove a surge in home buying that dried up much of the supply in the housing market. While timing is uncertain, rates will eventually decline and gradually bring buyers back to the table while also supporting a stable supply.

The value of Norway’s sovereign wealth fund rose 6.3% last quarter, adding a whopping $110 billion to the country’s stockpile despite technically falling just shy of its target benchmark return.

What started as the Norwegian government’s rainy day fund — somewhere to put its excess oil revenues in the 1990s — has become the largest investor on the planet. Today, 71% of its investment portfolio is in equities: a total of $1.1 trillion spread across more than 8,800 companies in 65 countries. Mirroring a diversified market index due to its sheer size, the fund has slices of every major sector. Visualized above are ~4,900 of the fund’s equity investments: the smallest dots in the chart, the ones that you can barely see, represent $10 million stakes in individual companies.

Keeping it public

But, while its equities portfolio returned a respectable 9% in Q1, its fixed income and unlisted real estate investments saw losses, pulling down the overall return. Indeed, in the past 2 decades, the fund’s equity investments have grown some 21x in value — and its success in public stocks is one reason why the Norwegian government last week confirmed it wants nothing to do with private equity, even as other institutional investors increase their exposure to the asset class.

In case managing this behemoth portfolio wasn’t enough, you can catch the fund’s chief hosting his podcast, where he interviews the likes of Elon Musk and Satya Nadella — two CEOs of companies that the fund owns a large slice of.

Slippery slope: When you’re managing a pot of $1.6 trillion, even a tiny Excel error can result in a $92 millionmiscalculation.

Development is nothing new to the Lakewood Ranch area, but a development that includes affordable housing units is now on the horizon.

Windham Development submitted an application to Manatee County to build 66 townhomes on a 10-acre parcel located at 3518 Lorraine Road.

If approved, 25% or 17 of the townhomes will be rented at a “moderate affordable” rate as determined by the Department of Housing and Urban Development.

The project was recommended unanimously by the Planning Commission on April 11. It will go before the Board of County Commissioners on April 18 at the land use meeting.

The yellow rectangle shows the 10-acre site where Windham Development wants to build 66 townhomes.

Amara, the county’s first affordable housing project approved in East County, was approved in January. The project will provide 152 units of affordable housing on Lena Road about a mile south of S.R. 64.

If approved, Lorraine Crossings will offer the first affordable units in the Lakewood Ranch area. Savanna at Lakewood Ranch is located to the north and west of the property, and Esplanade at Azario is to the east.

What is affordable housing?

Affordable housing is not Section 8 housing. These are not government-run apartments. The apartments are in standard developments, but at least 25% of the units are guaranteed not to exceed HUD’s rental cap for a set number of years.

In the case of Lorraine Crossings, 17 units must remain rent controlled over a period of 20 years. Rowena Young-Gopie, Housing Development Coordinator for Manatee County, said that the rest of the units are priced at market rate by the developer.

The word “affordable” is subjective given the location of the rental. Manatee County’s median income is $97,000, one of the higher medians in the state. Meanwhile, neighboring DeSoto County is on the lower end of the scale at $57,100.

Depending on the number of bedrooms a unit has, the difference between the two medians results in a $500 to $1,000 difference in rent caps. A studio apartment in Manatee has a higher rent cap than a two-bedroom in DeSoto.

HUD rental limits by number of bedrooms

% of Median Income

0

1

2

3

4

5

30%

$453

$486

$583

$752

$929

$1,106

50%

$756

$810

$971

$1,122

$1,252

$1,381

80%

$1,208

$1,295

$1,553

$1,795

$2,002

$2,210

120%

$1,815

$1,944

$2,331

$2,694

$3,006

$3,316

140%

$2,117

$2,268

$2,719

$3,143

$3,507

$3,869

For the Manatee workforce, that means even “affordable housing” in the area can be pricey. Rent caps are income-based, so a lessee earning 120% of the median could pay up to $2,694 a month for a three-bedroom unit in Lorraine Crossings.

For a family earning 80% of the median income, the rent would be capped at $1,795 a month for the same unit.

The affordable housing units at both Amara and Lorraine Crossings are designated for applicants earning from 80-120% of the median income of $97,000.

HUD household income limits by number of people

% of Median Income

1

2

3

4

5

6

30%

$21,150

$24,150

$27,150

$31,200

$36,580

$41,960

50%

$35,200

$40,200

$45,250

$50,250

$54,300

$58,300

80%

$56,300

$64,350

$72,350

$80,400

$86,800

$93,250

120%

$84,480

$96,480

$108,600

$120,600

$130,320

$139,920

140%

$98,560

$112,560

$126,700

$140,700

$152,040

$163,240

Under those percentages, a family of five can earn up to $130,320. But could that family of five afford an apartment even on the low-end of the rent scale? The Bureau of Economic Analysis estimates the average annual cost of living in Florida is $50,689 per person.

“In my opinion, I don’t think of $1,800 as affordable,” Coldwell Banker Realtor Chris Schwartz said. “You have $1,800 plus water, electricity, cable and internet. And now, you need a car to drive around. Then you need gas and have to eat. And if you have children, there’s daycare expenses.”

Who benefits?

The county’s intent is to provide more affordable housing options for residents, but the high median income poses a challenge because that’s the number the rent and income caps are derived from.

“We don’t create this calculation, we just adhere to HUD rules,” Young-Gopie said.

Looking at the rental market, what’s being proposed as “moderate affordable” by HUD can be found outside these deals brokered by Manatee County.

Developers are incentivized to include affordable housing in their developments through the Livable Manatee program, which was passed in 2017 and revamped in 2022.

Developers benefit from the program through higher density allotments, expedited permitting and design leeway for parking, buffers and access points.

To date, developers in East County have only signed deals to serve residents earning between 80-120% of the median income. So on the high-end, the caps are competitive within the current market.

Lorraine Crossing isn’t approved or built yet, but as of today, large families earning 120% of the median income could find a bigger bang for their buck next door in Savanna.

Single family homes with four bedrooms and up to three bathrooms are listed for rent on Homes.com for less than HUD’s high-end rent cap of $3,006 for a four-bedroom.

Two apartment complexes near the proposed site for Lorraine Crossings, Vida Lakewood Ranch and Estia at Lakewood Ranch, start two-bedroom apartments at less than HUD’s rate for those earning 120% of the median income in that category, too.

However, if comparing Vida and Estia to an affordable unit at the 80% income level, there is a savings. Two-bedrooms start at about $2,200 in both complexes, and the HUD cap is $1,553 for that income bracket.

Vida and Estia are luxury apartment complexes that come with heated pools and fitness centers among other amenities. Lorraine Crossings and Amara will be standard housing.

Planning Commission Chair Richard Bedford asked Windham to find room for a “tot lot” at Lorraine Crossings.

“Since it’s an affordable housing project, one would assume there’s going to be some children running around,” Bedford said. “Maybe between now and the board hearing, you might want to entertain that.”

The county is widening Lorraine Road from two lanes to four between 59th Avenue East and State Road 64. The county needs about a third of an acre along Lorraine Road to complete the improvements.

Because Windham plans to include affordable housing, the project was able to bump up the density from 3 dwelling units per acre to 6.85 units per acre.

In between the road and wetlands, the 66 townhomes will be built within nine buildings at a maximum of two stories. A two-lane street will run through the center of the complex to provide access from Lorraine Road.

If approved, construction is expected to begin in the first or second quarter of 2025.

Federal Reserve officials signaled a more sober tone this week, emphasizing that they’re in no rush to cut interest rate cuts this year.

On Tuesday, Fed Chair Jerome H. Powell laid out his case for why borrowing costs could stay higher for longer than the central bank expected just a few weeks ago. Since the start of the year, Powell and his colleagues had said they were looking for more assurance that inflation was ticking steadily down. Instead, they’ve gotten the opposite.

“The recent data have clearly not given us greater confidence, and instead indicate it’s likely to take longer than expected to achieve that confidence,” Powell said Tuesday at a panel discussion on the U.S. and Canadian economies.

Plus, the rest of the economy has stayed remarkably resilient after interest rates climbed to the highest rate in decades. The job market continues to grow at a surprising clip. And that means the Fed can stay focused on zapping inflation, without worrying that its fight is eroding business’ willingness or ability to hire, or people’s ability to find stable jobs. Put together, the data on inflation and jobs mean it is “appropriate to allow restrictive policy further time to work,” Powell said.

The message was echoed earlier in the morning by Powell’s No. 2. In a speech, Fed Vice Chair Philip Jefferson said that if upcoming data suggests inflation is “more persistent” than he expects, it would make sense to keep rates higher for longer.

Powell and Jefferson did not get specific on the timing of upcoming cuts or exactly how many there will be. Last month, when central bankers sketched out their expectations for the path ahead, they penciled in three cuts before the end of the year.

But Fed watchers and the financial markets are now questioning not just when cuts will happen, but also if the Fed will be able to eke out even one or two cuts. The outlook shifted considerably last week after March inflation data came in hotter than expected, cementing fears that a new trend had taken hold.

Now that Fed officials have gotten three months of disappointing news, economists assume they’ll need as much encouraging news — at the very least — to put them back on track to cut rates. That means even the most optimistic scenarios don’t include a cut before late summer.

“There’s absolutely, in my mind, no urgency to adjust the policy rate,” San Francisco Fed President Mary Daly said last week. “Policy is in a good place right now, and I need to be fully confident that inflation is on track to come down to 2 percent — which is our definition of price stability — before we would consider a rate cut.”

U.S. credit card delinquency rates were the highest on record in the fourth quarter of 2023, according to the Federal Reserve Bank of Philadelphia. 3.5% of card balances were at least 30 days late as of the end of December. The number of people making minimum payments also rose, pointing to distress among cardholders. While 25% of active accounts have a balance of over $2,000 for the first time, one third of users pay their balance in full every month, exhibiting contrasting behaviors from likely different brackets of earners.

Issuers have responded to the rise in delinquencies by lowering the credit limit on new accounts. The problem is a direct result of the higher cost of living for Americans, as the last few inflation prints illustrated stickier than expected inflation. The Fed is unwavering in its goal to lower inflation, and their hope is that higher rates will eventually slow spending and reduce inflationary pressures. A higher for longer environment will help regulate the economy and the credit card delinquencies are an unfortunate symptom of the Fed’s remedy for inflation.

I could see this information permeating into tenants lives and thus into ownerships lives as tenants may begin to struggle with payments, rent increases, higher utility costs or additional fees.

If you would like to discuss the markets, or need some guidance for just about anything related to income producing properties including Property Management Rockstar Companies, Electricians, Insurance Providers, Landscaping, or just a plain old valuation and analysis for selling your asset(s), then you’ve found the right guy, so let’s connect!

You must be logged in to post a comment.